Debits & Credits Explained

By Travis Bacon

December 16, 2020

The first thing you need to understand is that the universal concept of double-entry bookkeeping which uses debits and credits is originally a made-up system. The whole idea is to create a balance between two sides of a transaction. (i.e. when you purchase an item the money has come from the bank: the item purchased should balance with the bank transaction). Ultimately each transaction must be done in exchange for something of equal value.

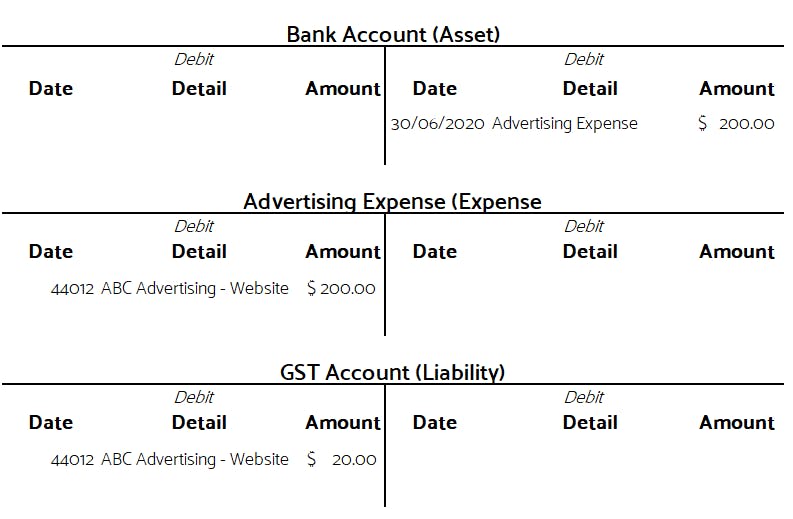

You may Remember the old t-ledgers as school, which are used to visualise the balance of a transaction. (Debits are always on the left, credits are still on the right). Consider the following transaction, $220 paid to ABC Advertising for website expenses.

- The bank account is reduced by $220.00

- The Advertising Expense is increased by $200

- The GST amount refundable from the ATO is debited to the GST account.

This transaction is balanced.

The question that often comes next is; How do you know if it should be a Debit or Credit?

There is an acronym that has stuck with me since grade 8 accounting: DEALOR.

DEALOR represents each type of transactional account and identifies the increasing nature of an account type.

Nature of an account example:

- To increase the bank account, a debit entry would exist, to decrease the bank account, a credit entry would exist.

- The opposite applies to a bank loan, as it is Credit by nature, then reducing the loan is a debit transaction.

This makes sense – if you take money out of the bank and pay your loan, your bank is decreased (credit transaction) and your Loan decreases (debit transaction). I.e. Credit = Debit the transaction is balanced.

Let's take a closer look at the transaction account types using the acronym. (DEALOR)

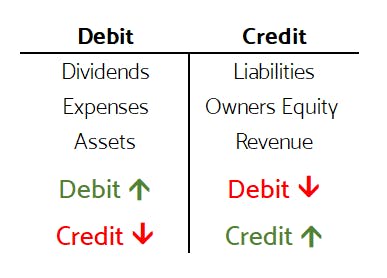

Dividends/Distribution (Debit in nature)

These accounts represent the money paid out of yearly profits or retained profits to shareholders, beneficiaries of trusts and partners in partnerships.

You may see some of the following names in your financial statements:

- Dividends

- Dividends paid

- Distributions

- Trust Distributions

- Partner Distribution

Expenses (Debit in nature)

These are costs related to the day to day operation of a business.

Some examples of "Expense" accounts are::

- Advertising

- Cost of Goods Sold.

- Rent

- Travel

- Salaries

Assets (Debit Nature)

Assets are items that provide a future economic benefit to a company.

Some examples of "Asset" accounts are:

- Cash

- Accounts Receivable (Debtors)

- Inventory

- Prepaid Expenses

- Property and Equipment

- Vehicles

Liabilities (Credit Nature)

Liabilities are the obligations that and entity is required to pay, such as supplier invoices.

Some examples of "Liability" accounts are:

- Accounts Payable (Creditors)

- Income Tax Payable

- GST Liability

- Loans/Hire Purchases

Owners' Equity (Credit Nature)

These accounts represent the net asset of the entity (i.e. Assets minus Liabilities = Owners Equity)

Examples of "Owners' Equity" accounts are:

- Retained Earnings / Profits

- Share Capital

- Settlement Sum

- Accumulated Other Comprehensive Income

Revenue (Credit Nature)

These accounts represent the income earned from the sale of goods, services and/or income from various investments.

Some examples of "Revenue" accounts are:

- Sales

- Interest Income

- Investment Income

Modern accounting systems, like Xero really, actually make it possible to do your bookkeeping without fully understanding your debits and credits. When things go wrong, and yes, even things can go wrong in an online accounting system, it is handy to be able to go back to the debits and credits of a transaction.

TaxDigital offers training solutions for modern accounting systems, and we can also help you understand how those systems deal with Debits & Credits. We look forward to nerding out with you!